That didn't occur, and the memory of the outcome has actually continued to be clear. Interest-only ARMs as well as choice ARMs are other means homebuyers can begin with low settlements however wind up with much greater settlements down the road. You have actually reached take note of changes in the fed funds price and also temporary Treasury costs returns, since LIBOR usually alters in lockstep with it. A variable-rate mortgage is a lending that bases its interest rate on an index, which timeshare presentation deals 2020 las vegas is normally the LIBOR rate, Check out here the fed funds rate, or the 1 year Treasury bill. An ARM is additionally referred to as an "adjustable-rate car loan," "variable-rate mortgage," or "variable-rate loan." However, there are some types of car loans that she would certainly recommend homebuyers prevent.

It deserves keeping in mind that ARMs make up 18% of all home mortgages in California, a confirmation that in the most expensive edges of a pricey market, individuals should be as calculated as possible. The pair had actually been outbid on the initial residence they tried to buy as well as really did not wish to take the chance of losing once more. So when they put in an offer on the townhouse, they bumped it to $30,000 above the asking price, although the repayments might stress their budget. That became troublesome, nonetheless, when the real estate market crashed as well as the ARMs reset to higher rates that those customers could not handle. If your concept of huge threat is biting into a truffle without asking what taste it is, you probably want a longer set period. If you have actually obtained a five-year plan, for example, a 7/1 ARM could aid you sleep a little better in the evening.

- Accessibility to Electronic Providers may be limited or unavailable during durations of peak demand, market volatility, systems update, maintenance, or for other reasons.

- Lots of people select ARMs since they a minimum of in the starting charge less passion than a fixed-rate home loan.

- Along with knowing just how often your ARM will change, consumers need to recognize the basis for the modification in the rate of interest.

- Interest-only loans are very uncommon, and also customers that desire an ARM usually need higher credit history as well as need to put even more cash down than buyers that want a fixed-rate home mortgage.

- Your lender chooses which index to base your price on when you get the car loan, but the LIBOR is one of the most popular index made use of.

It suggests that the quantity you owe rises, also as you pay. It occurs when the amount you pay isn't sufficient to cover the interest on your lending. The difference between the two is added to the equilibrium of your funding and also rate of interest is charged on that. The result is that you might owe more a couple of months into the funding than you did at the start. Ask your lender if there is a possibility of negative amortization in your funding. The finance may be offered at the loan provider's common variable rate/base price.

Should You Pay Off A Home Loan Prior To You Retire?

The rates of interest for a variable-rate mortgage is a variable one. The preliminary rate of interest on an ARM is established below the market price on an equivalent fixed-rate lending, and then the rate rises as time goes on. If the ARM is held enough time, the interest rate will surpass the going rate for fixed-rate financings. Fixed-rate home mortgages and variable-rate mortgages are both primary mortgage types. While the industry offers numerous ranges within these 2 classifications, the primary step when shopping for a home mortgage is figuring out which of both major car loan types ideal suits your demands. Even worse, those car loans frequently had preliminary rate home windows as short as one year and could have synthetically low "teaser prices" that would increase when the first set duration finished.

Dealt With

The hybrid ARMs are the most popular selection of the three types used, mostly since they are the simplest to recognize as well as most practical for new property buyers, yet Vogel provides a caution. If you are just getting started in the workforce as well as homebuying market, every buck counts as well as ARMs can save a few bucks, a minimum of up until the dreaded modification period kicks in. Whether you choose a fixed-rate mortgage or an ARM, do not be enticed right into obtaining greater than you can afford. Pros include low initial prices as well as flexibility; cons include intricacy and also the possibility for much bigger payments in time. Nonetheless, if you're buying what you plan to be your irreversible home, a fixed-rate home mortgage is probably your better option.

An ARM index is what loan providers use as a benchmark rate of interest to identify exactly how variable-rate mortgages are valued. Let's state you are looking for your very first home as well as simply graduated from clinical or law school or made an MBA. The possibilities are high that you are going to gain extra in the coming years and will certainly have the ability to pay for the enhanced repayments when your lending adapts to a higher price. In one more scenario, if you expect to begin receiving money from a trust fund at a specific age, you might obtain an ARM that resets in the exact same year.

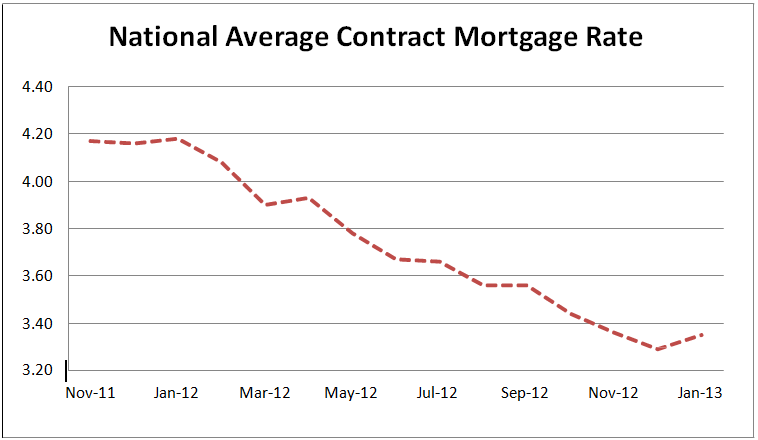

Over the last few years, with interest rates hovering at document lows, customers who had an adjustable-rate mortgage reset or adjusted really did not see as well large an enter their month-to-month repayments. Yet that can change depending upon how much and also just how rapidly the Federal Get increases its benchmark rate. So as to get a grasp on what remains in store for you with an adjustable-rate mortgage, you first need to understand exactly how the item works.

Loaning requirements are stricter today than during the 2006 housing bubble, Rugg kept in mind. In the real estate run-up greater than a years ago, some lending institutions distributed supposed "phony's lendings," or home mortgages that required little or no documents of revenue. Today, banks need customers to verify their revenue to qualify for a funding. But financial experts say there are some distinctions between today's pandemic real estate boom as well as 2006, such as banks' stricter lending standards. They include interest-only home loans, where debtors pay just the rate of interest on their lending for the very first 3 to one decade. She's likewise not a follower of payment-option ARMs, where borrowers can pay much less interest than they owe for that passion getting added to the principal.

Top 6 Home Loan Blunders

There might be a direct as well as legally specified link to the underlying index, but where the lending institution uses no particular link to the underlying market or index, the price can be transformed at the loan provider's discernment. In several nations, flexible price home loans are the norm, and in such areas, might merely be described as home loans. A lot more buyers are picking adjustable-rate mortgages, which supply reduced month-to-month payments originally, to emulate record-high home rates. Those reduced regular monthly repayments, as opposed to traditional 30-year fixed-rate home mortgages, are confirming to be a solid attraction for customers aiming to afford a house in the white-hot housing market.

For lots of people, the initial what happens to timeshare when owner dies fixed-rate period matches how long they'll remain in their home prior to they relocate or refinance. Germain Depository Institutions Act of 1982 enabled Flexible price mortgages. Option ARMs are best suited to sophisticated debtors with growing incomes, specifically if their revenues fluctuate seasonally and also they require the repayment flexibility that such an ARM might supply. Innovative consumers will carefully handle the degree of adverse amortization that they permit to accumulate. The contract with the loan provider may have a stipulation that allows the customer to transform the ARM to a fixed-rate home loan at marked times.